1. What would the 5-year forecast look like with the proposed decrease of the existing 1.25% earned income tax to 0.75% and an additional 0.5% earned income tax going to the general fund (an increase of $1.2 million in the projection below)?

A board member stated that this scenario is legally not possible due to the terms of bond repayment. I do not have the legal knowledge or access to the bond repayment terms to dispute this statement.

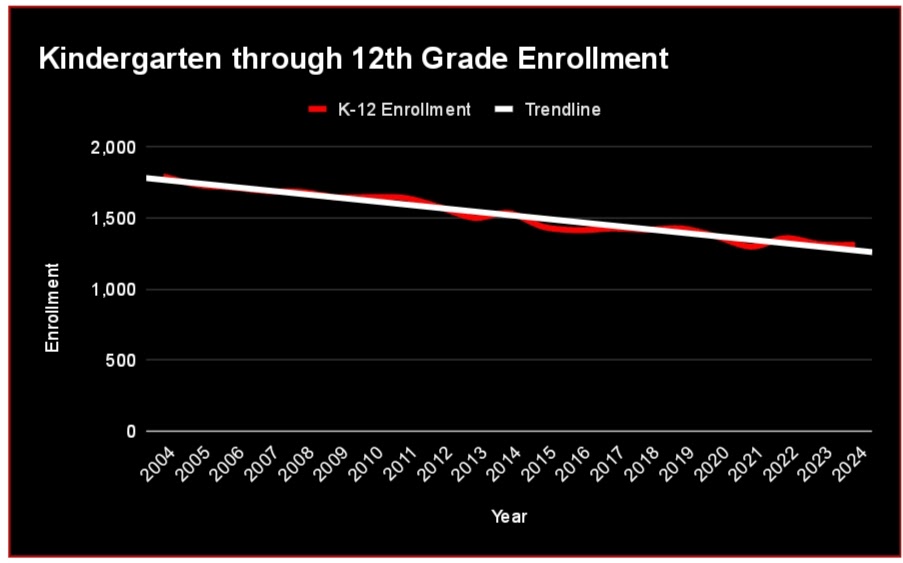

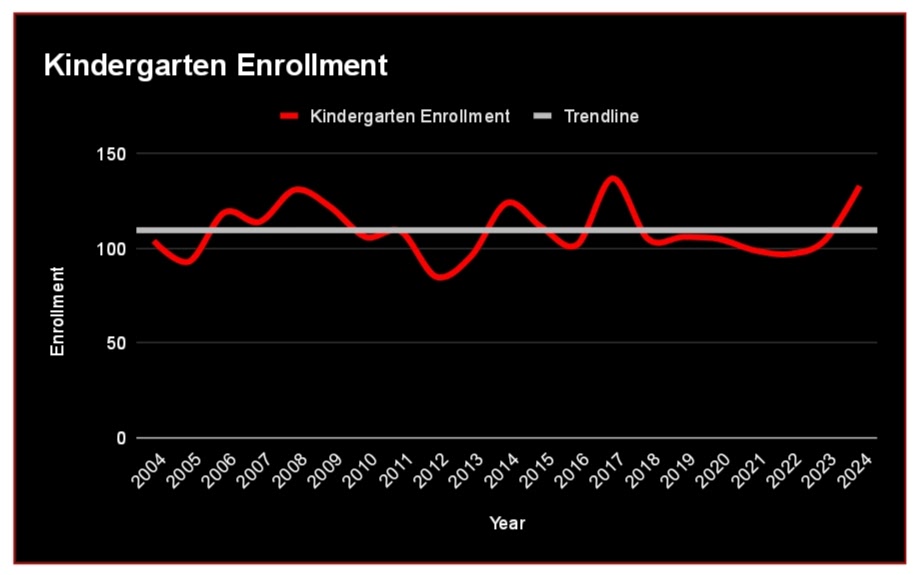

2. Was the board informed that purchasing the land across the street from the school was necessary due to increasing enrollment? Could I review the data that supports this enrollment growth trend?

Below is the data I obtained from the state for the past twenty years. I observe a declining trendline for K-12 enrollment and a flat trendline for kindergarten enrollment.

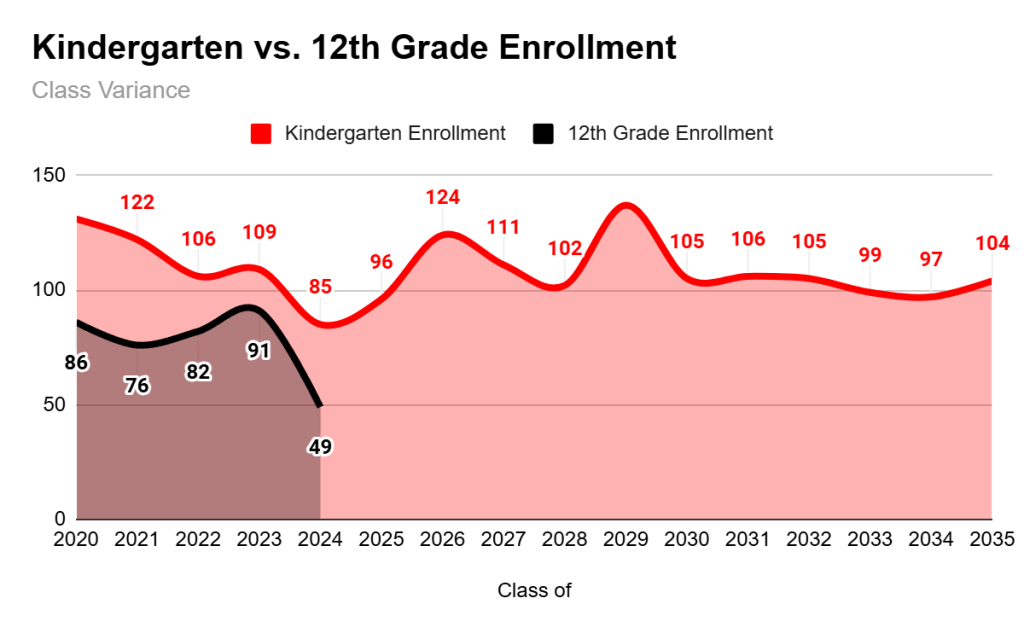

The following graph may be helpful to see the change in enrollment from kindergarten to graduating senior class.

No data-supported response was given. A board member commented that this would be considered an upward trend.

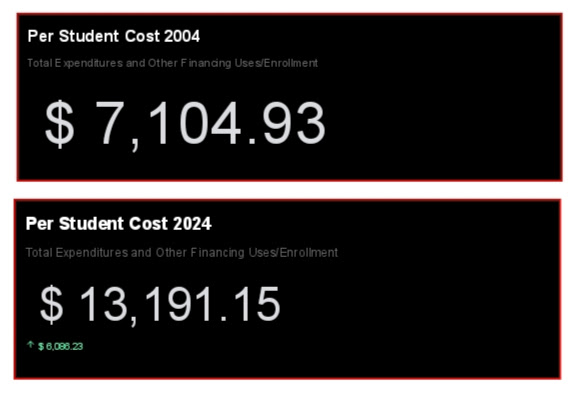

3. Why was the parallel drawn to compare our school district’s financial state to a person who had not received a raise in twenty years?

I tried to prove this was true also, but was unable to do so. I had to go to an analyst at the state in order to obtain the revenues and expenditures from 2004. I divided total expenditures by the enrollment from 2004 to calculate the per student cost from 2004: $7,104.93. Contrast this with the per student cost for 2024: $13,191.15.

I adjusted the per student cost for inflation over the last 20 years (66.3%) and calculated the per student cost for 2024 that we might be able to expect. It was still almost $1,400 lower than our actual spending.

And here’s the thing, the school district brought in enough revenue to spend $700 over that inflation-adjusted estimate, but it’s the remaining $700 per student that is putting us in the red.

No response has been received.

4. Why did we switch from a GAAP-approved method of accounting to a non-compliant cash basis in 2011 ?

Excerpt from 2011 Financial Statements (first year after switching to non-compliant cash-basis):

As a result of using the cash basis of accounting, certain assets and their related revenues (such as accounts receivable) and certain liabilities and their related expenses (such as accounts payable) are not recorded in the financial statements. Therefore, when reviewing the financial information and discussion within this report, the reader must keep in mind the limitations resulting from the use of the cash basis of accounting.

Source: Page 3

Excerpt from 2023 Financial Statements:

NOTE 2 – COMPLIANCE Ohio Administrative Code, Section 117-2-03(B), requires the School District to prepare its annual financial report in accordance with generally accepted accounting principles. However, the School District prepared its financial statement on a cash basis, which is a comprehensive basis of accounting other than accounting principles generally accepted in the United States of America. The accompanying financial statements omit assets, deferred outflows of resources, liabilities, deferred inflows of resources, net position/fund balances, and disclosures that, while material, cannot be determined at this time.

Source: Page 18

This type of note in a school district’s financial statements indicates that the district did not comply with the requirement to prepare its financial statements using Generally Accepted Accounting Principles (GAAP), as mandated by the Ohio Administrative Code.

Here are the key reasons why this note appears and what it implies:

Use of Cash Basis Accounting Instead of GAAP

- GAAP: Under GAAP, financial statements are prepared using an accrual basis of accounting, which recognizes revenues when earned and expenses when incurred. It requires a full accounting of assets, liabilities, fund balances, and related disclosures.

- Cash Basis: The district opted to use cash basis accounting, which records transactions only when cash is received or paid. This method is simpler but does not account for accruals like accounts receivable, accounts payable, and other deferred inflows/outflows.

Impact of Cash Basis Reporting

By preparing statements on a cash basis instead of GAAP, the financial statements omit significant financial information, including:

- Assets (e.g., buildings, equipment, receivables)

- Liabilities (e.g., loans, unpaid obligations)

- Deferred Outflows/Inflows of Resources

- Net Position/Fund Balances

These omissions mean the financial health and full financial position of the district cannot be accurately determined from these statements alone.

Compliance Issue

- The Ohio Administrative Code requires GAAP reporting to ensure transparency, consistency, and accountability for public entities like school districts.

- Noncompliance, such as using cash basis reporting, must be disclosed in the notes to alert readers that the financial statements do not meet the required standards.

Reasons for Using Cash Basis

While not explicitly stated, the district may have chosen cash basis accounting due to:

- Cost and resource limitations: Preparing GAAP-compliant statements requires more time, expertise, and financial resources. Smaller or resource-constrained districts may struggle to meet these demands.

- Simplicity: Cash basis is easier to understand and prepare, as it focuses solely on cash inflows and outflows.

Consequences of Noncompliance

- Potential for audit findings or concerns from regulatory bodies.

- Reduced confidence from stakeholders (e.g., taxpayers, bondholders) about the district’s financial position.

- Difficulty in securing grants or financing, as many entities require GAAP-compliant statements.

In summary, this note highlights that the district is not in compliance with Ohio’s GAAP reporting requirement, and it clarifies that the financial statements omit material information, limiting their usefulness for understanding the district’s full financial picture.

Search for audited financial statements here.

A board member suggested that the change was likely due to simpler methods and cost-saving measures.

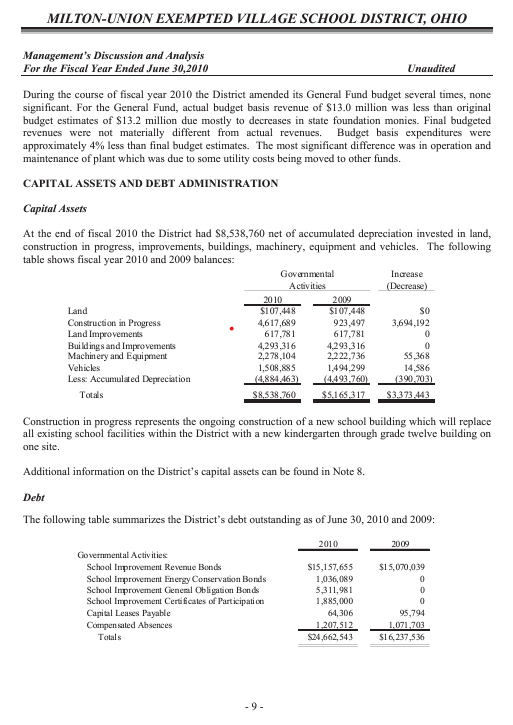

5. Per OAC 117-2-02, how can I view the district’s capital asset records?

The last one I can find is from 2010 when the district was still using a GAAP-approved method of accounting.

No response has been received.

6. Can we see the revenues and expenses as it pertains to open enrollment? I am aware that the funding formula changed in 2022.

No response has been received.

7. Are we concerned that the recent cuts to transportation and intervention services may disproportionately impact our economically disadvantaged students?

No response has been received.

8. Why is our Total Permanent Improvement Millage nearly double that of other local school districts I reviewed in the ODEW District Profile?

No response has been received.