Alternative Tax Document Information contains the alternative tax budget process for the Milton-Union Exempted Village School District (documented in the January Board Meeting Agendas), including guidelines, deadlines, and financial schedules required for tax revenue estimation and reporting.

Taxing District Information and Context

The Milton-Union Exempted Village School District is subject to specific tax budget regulations under Ohio law. The county budget commission has the authority to waive tax budget requirements for various taxing authorities.

Guidelines for Completing Alternative Tax Documents

The guidelines provide a structured approach for completing various schedules related to property tax revenues and expenditures. Each schedule serves a specific purpose in demonstrating financial needs and compliance with Ohio Revised Code.

- Schedule 1 demonstrates the need for property tax revenues.

- Schedule 2 provides an Official Certificate of Estimated Resources.

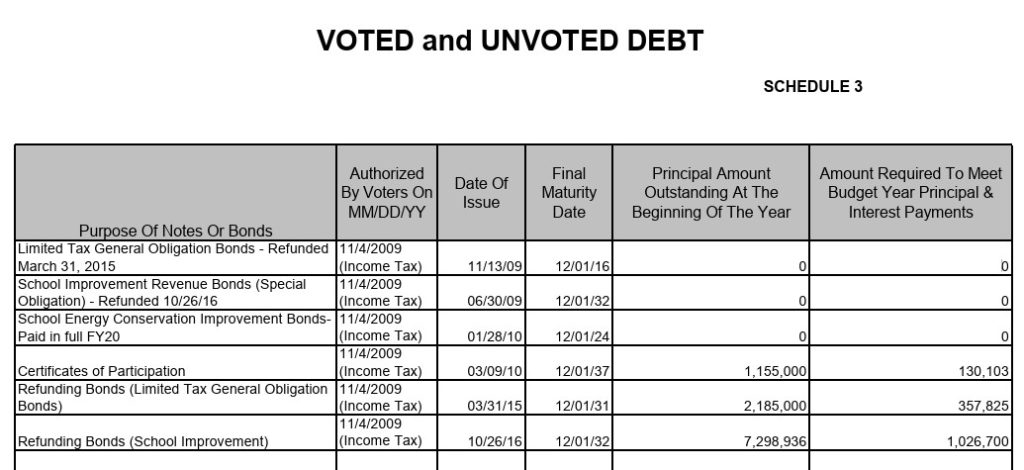

- Schedule 3 addresses debt service requirements for bonds.

- Schedule 4 ensures proper division of taxes levied.

- Schedule 5 accounts for tax anticipation notes.

Detailed Revenue Schedule for General Fund

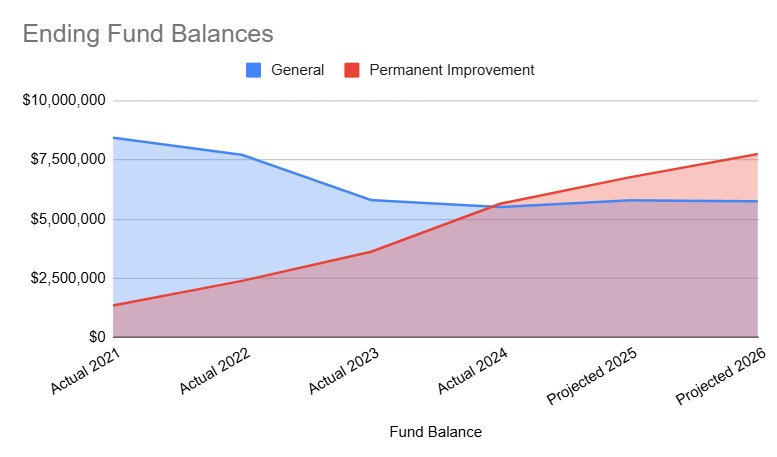

The General Fund’s financial data shows a projected increase in revenues and expenditures for the upcoming fiscal year. The ending unencumbered fund balance is expected to decrease slightly.

- Total revenue projected for FY 2026 is $16,492,034.

- Total expenditures for FY 2026 are estimated at $16,407,033.

- Ending unencumbered fund balance is expected to be $5,350,030.

Detailed Revenue Schedule for Permanent Improvement Fund

The Permanent Improvement Fund indicates a significant increase in the ending fund balance over the fiscal years. The fund’s revenues are primarily driven by property taxes and income tax.

- Total revenue for FY 2026 is budgeted at $3,917,268.

- Total expenditures for FY 2026 are estimated at $2,900,516.

- Ending unencumbered fund balance is projected to be $7,146,039.

Debt Service Funds Overview

The debt service funds section provides an overview of the financial status related to debt obligations.

- Bond/Note Retirement: Amount required to meet budget year principal & interest payments (in chart below) sums to $1,514,628.

Recommendation: Evaluation and Rebalancing of General and Permanent Improvement Fund Allocations

Background:

A review of the Alternative Tax Budget Documents, including actual and projected fund balances, reveals a notable inverse relationship between the General Fund and the Permanent Improvement (PI) Fund.

Concern:

If this trend continues, we may encounter a disproportionate allocation of resources, potentially limiting the district’s flexibility to respond to rising instructional costs, staffing needs, or state funding changes. Additionally, proposed legislation such as Ohio House Bill 96, which seeks to cap General Fund reserves at 30% of the previous year’s operating expenses, may further restrict our ability to manage surplus balances efficiently.

Recommendation:

It is recommended that the Board of Education consider a comprehensive review of current income tax allocations and long-term funding strategy. Specifically:

- Explore the feasibility of a Board resolution (similar to this one) to reduce the existing 1.25% earned income tax rate, particularly in light of the recently passed 0.75% increase dedicated to the General Fund.

- Develop a multi-year funding model that includes reserve targets, strategic investment priorities, and potential levy adjustments to better balance capital and operational needs.

- Communicate transparently with stakeholders regarding fund usage, rationale for adjustments, and long-term benefits to district financial health and educational quality.

This proactive approach will help ensure sustainable financial stewardship while continuing to support both instructional excellence and facility maintenance.